Today’s money world presents investors with a demanding environment. But even while markets are rough to interpret right now, and volatility has greater as a end result, a clever investor can nevertheless obtain stocks that are offering the merchandise. From time to time, very practically.

Two shipping company shares have been exhibiting superior share rate appreciation in recent months. These are sustained gains, that have much outpaced the S&P 500’s year-to-date efficiency. While we all know that past general performance will not warranty upcoming success, the greatest location to commence hunting for tomorrow’s high-advancement stocks is among yesterday’s winners.

We ran the tickers via the TipRanks databases to get a sense for what the Road has in thoughts for these names turns out both of those are rated as Sturdy Buys. Let’s acquire a nearer glimpse.

Ardmore Delivery (ASC)

In enterprise since 2010, Ardmore is a shipping firm offering voyage charters, time charters, and commercial pool vessels. The company’s fleet of 25 solution and chemical tankers averages only 6 several years of age, making it one of the industry’s most modern-day. In retaining with its determination to keeping a modern-day fleet, in early April Ardmore introduced the sale of three vessels – all built in 2008, and so very well more than the fleet’s typical age – to Leonhardt & Blumberg. The sale, for $40 million, will net Ardmore some $15 million in money proceeds.

Ardmore focuses on the transportation of petroleum products and solutions and other substances to customers around the globe. Its tanker fleet ranges from 25,000 to 50,000 deadweight tonnes, and its rather young age can make it additional fuel-effective than is generally uncovered in the business, an benefit for Ardmore at a time of increasing gas rates.

Year-to-day, shares in ASC are up 83%. The corporation has managed this even however quarterly revenues have not nonetheless returned to pre-COVID levels. In the most latest quarter documented, 4Q21, Ardmore had $52.5 million at the major line. This was up 25% calendar year-over-yr, but was nevertheless down 13% from the fourth quarter of 2019, in advance of the pandemic. The company ran a quarterly web decline of 25 cents, in line with expectations and a 35% enhancement from the calendar year-in the past quarter. Ardmore finished 2021 with $67 million in offered liquid assets, a whole that integrated $55.4 million in cash and income equivalents as effectively as $11.6 million in undrawn credit history.

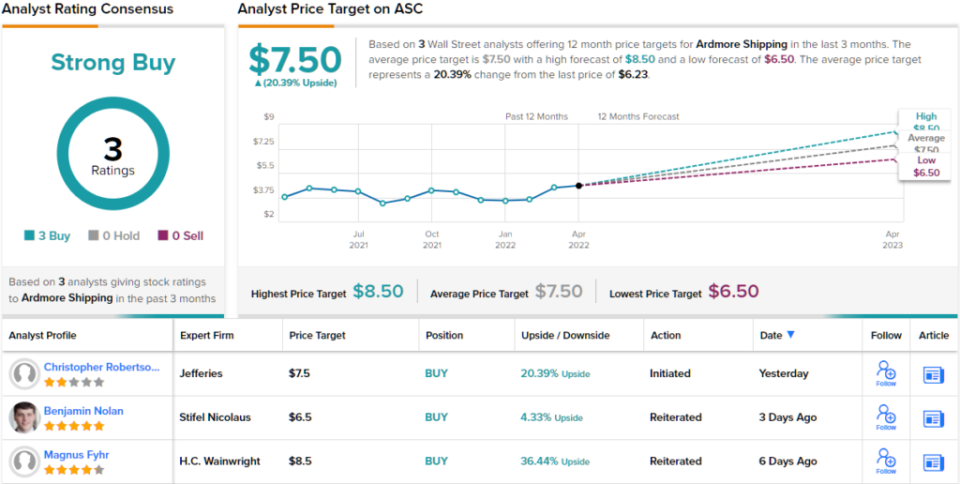

Covering this stock for H.C. Wainwright, shipping field pro Magnus Fyhr takes an upbeat stance. He notes that the company’s shares are mounting, and writes, “Despite the appreciation, we imagine ASC is attractively valued buying and selling at a 40% low cost to our believed NAV in comparison to an 18% discounted for the tanker peer team. In addition, with the merchandise tanker marketplace restoration getting momentum, we think the risk/reward stays appealing. Also, with a high-high-quality fleet, we imagine Ardmore is properly positioned to capitalize on stricter environmental regulations as older tonnage is marginalized.”

In line with these opinions, Fyhr charges ASC a Acquire along with an $8.50 cost focus on. Added gains of ~36% could be heading investors’ way should the concentrate on be achieved above the upcoming 12 months. (To enjoy Fyhr’s observe document, click on listed here)

Smaller-cap shippers like Ardmore do not always get the attention they may ought to have – but all 3 of the analyst assessments right here are good, earning the Robust Obtain consensus rating unanimous. ASC shares are priced at $6.24 and their average focus on of $7.50 indicates a a single-yr upside of ~20%. (See ASC stock forecast on TipRanks)

Global Seaways (INSW)

Up coming up is Intercontinental Seaways, a different modest-cap shipper – but a step up in measurement, as Global offers a sector cap of $1.1 billion. Worldwide owns and/or operates a fleet of 88 vessels, ranging in dimensions from 36,000 deadweight tonne (DWT) handymax tankers to giant 300,000+ DWT quite huge crude carriers (VLCCs) and to two even bigger 432,000 DWT floating storage and offloading (FSO) vessels. The enterprise focuses its operations on the carriage of crude oil and petroleum items on the world-wide sea lanes.

When compared to pre-pandemic ranges – that is, to 2019, prior to the supply chain and trade disruptions commenced – International’s revenues stay depressed. On the other hand, they are rebounding from the lows strike throughout the COVID disaster, and registered sequential quarterly gains in 2H21. The corporation completed very last year with a 4Q top line of $93 million, up an outstanding 75% 12 months-about-yr. For 2021 as a total, International posted revenues of $255.9 million. While this was down 36% y/y, it is critical to take note that the company’s revenues bottomed out in 1Q21, and have been trending up considering the fact that then.

In yet another position of significance for investors, International has understood some $25 million in value synergies in the 1st several months of 2022, connected to the company’s merger past 12 months with Diamond Transport. That merger built Worldwide one particular of the biggest diversified tanker corporations to be stated on the US markets.

All of this has caught the eye of Stifel’s 5-star analyst Benjamin Nolan, who described Intercontinental Seaways as a person of his ‘favorite names’ in tankers. Receiving into specifics, Nolan writes, “While the tanker marketplace has been weak, oil demand from customers is recovering. The Russia-Ukraine conflict has pushed limited time period tanker prices materially better, but longer term in the absence of price associated oil need destruction, we anticipate marketplace circumstances need to make improvements to considerably. With a large fleet benefiting from value synergies and fantastic fleet float, a robust stability sheet, and with shares trading at 82% of NAV, we assume there to be ongoing upside as the tanker current market recovers…”

Dependent on all of the earlier mentioned components, Nolan prices INSW shares a Purchase along with a $13 cost goal. Consequently, the analyst expects the inventory to modify fingers for ~21% top quality over the following 12 months. This is on best of the 53% development the stock has noticed this yr. (To view Nolan’s observe report, simply click right here)

Nolan is bullish in this article, but the 4 unanimously positive opinions on file exhibit that the Street agrees with this stance. INSW’s shares are buying and selling for $22.28 and their $27.50 ordinary price concentrate on indicates ~23% upside this calendar year. (See INSW inventory forecast on TipRanks)

To discover fantastic ideas for stocks trading at desirable valuations, take a look at TipRanks’ Best Shares to Purchase, a recently introduced tool that unites all of TipRanks’ fairness insights.

Disclaimer: The thoughts expressed in this report are entirely individuals of the highlighted analysts. The content material is intended to be utilized for informational applications only. It is really essential to do your have examination ahead of generating any financial investment.