Table of Contents

Wang He/Getty Images News")

Thesis

JD.com (JD) is a behemoth – from whichever way you look at it. It is the largest retailer in China and the largest internet company in China by revenue.

Aside from its already impressive growth in recent years, JD has established itself as the preferred platform when it comes to delivering authentic goods and good customer services via an unmatched fulfilment network.

This sets it up well to capitalize on the growing buying power of Chinese consumers.

Overview

JD.com was founded in 1998 by Richard Liu, who is still the controlling shareholder, CEO and Chairman of the Board. It was originally an offline-only store. The SARS outbreak in 2003 led Richard to shift the business online, and soon afterward, he began building the logistics side of the business. Further expansion in 2010 led to the forming of an online marketplace.

From the get-go, JD had a goal to supply the Chinese consumer with authentic, quality goods. This focus on authenticity remains a core characteristic today, putting it on a different level in a country where counterfeit goods are common.

I believe JD finds itself in a particularly strong position and well-aligned with one of the CCP’s stated key strategies – as communicated during the 14th Five Year Plan for National Economic and Social Development for the period 2021-2025, namely “Accelerating Digitalization and Constructing Digital China”. There is certainly a case to be made that JD – with its proprietary, smart supply chain technology will be able to play a key role in the CCP’s stated objectives in the coming years.

Financial Overview

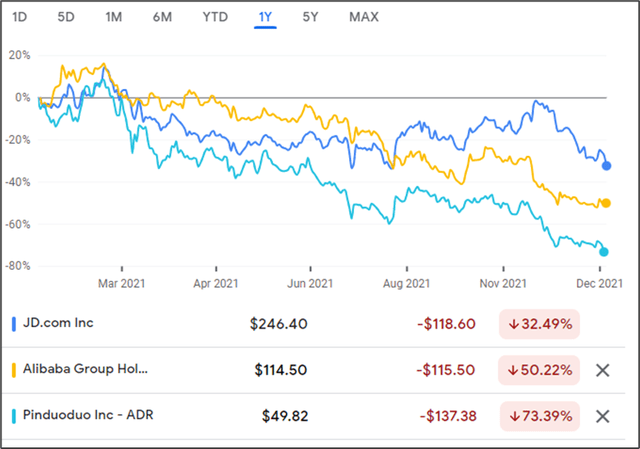

Zooming out a bit and taking a view of Chinese e-commerce performance recently does not paint a pretty picture. It has been a tough year, with JD, Alibaba (BABA), and Pinduoduo (PDD) all shedding more than 30% in 2021.

Google Finance

The weak performance can primarily be attributed to the Chinese regulatory environment and all the uncertainty surrounding it, ranging from concerns about Beijing’s common prosperity drive to the legality of the widely used VIE (Variable Interest Entity) structure and delisting fears in the US.

It seems JD believes the weakness in its share price is unjustified. In late December 2021, they announced plans to boost their current $2 billion share buyback program by 50% to $3 billion. JD’s willingness to act (in only its second year of profitability) on what they believe to be an undervalued share price is an encouraging sign for investors.

Taking a high-level overview of JD certainly paints an impressive picture:

- More than 550 million annual active customers;

- Fulfillment operation covering 99% of the Chinese population;

- Delivering 90% of ordered packages on either the same or next day;

It quickly becomes clear that management knows a thing or two about running a large enterprise.

The company has an extremely strong balance sheet, with total investments of RMB 99.6 billion versus total debt of RMB 15.8 billion at the end of 2020.

ESG Overview

JD’s role in advancing the poorer, rural parts of China through initiatives like a dedicated section of their e-commerce platform designed to sell products from rural areas certainly scores it some brownie points from Chinese authorities.

Tellingly, in 2017, Richard received “The Contribution Award for Poverty Alleviation” from the Chinese government.

There are some issues to be noted, though – such as this mugshot. Not ideal for anyone, especially the CEO of a major international company.

Richard’s squeaky clean image was cast under immense scrutiny after he was accused of raping a Chinese student in the US in August 2018. He maintains all relations were consensual.

Liu was released and prosecutors decided not to pursue the case because of insufficient evidence. A lawsuit was filed and the case is still ongoing. Any further potential fallout might be damaging to JD.com – which is also listed as a defendant in the case.

Breaking Down the Business

Following changes in the organization’s structure, JD now reports using the following segments (since Q121):

- JD Retail

- JD Logistics

- JD New Businesses

JD IR

JD Retail

This is the backbone of the JD empire – responsible for generating 87% of revenue during FY2020. This number has been steadily declining, having represented 92% of total revenue during FY2016.

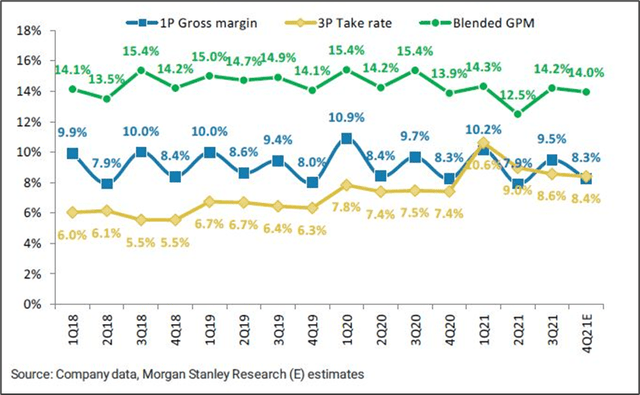

For the first few years of its existence, JD was purely a 1P player with a heavy focus on electronic goods. In 2010, JD branched out to offer a 3P marketplace. It places the same strict standards on its 3P marketplace than on its 1P platform – again, trying to ensure the authenticity of goods, level of customer service and overall experience that consumers receive is on par with its own offering.

During recent quarters – the growth of the 3P platform has been faster than that of the 1P platform, likely in part due to the ban of Alibaba’s “2-choose-1” system – which enabled merchants already listed on Alibaba to open stores on JD’s marketplace as well. Margins within the 3P sector are generally much higher than in the 1P sector – and thus the overall effect of stronger 3P growth will be accretive to JD’s overall margin profile.

Morgan Stanley

JD vs. Others – what are the differences?

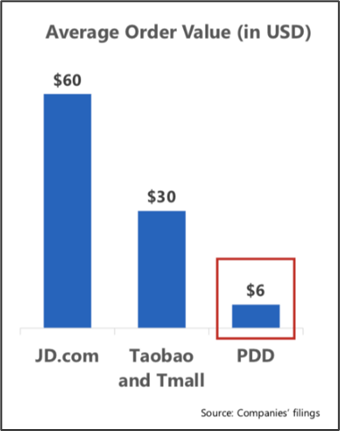

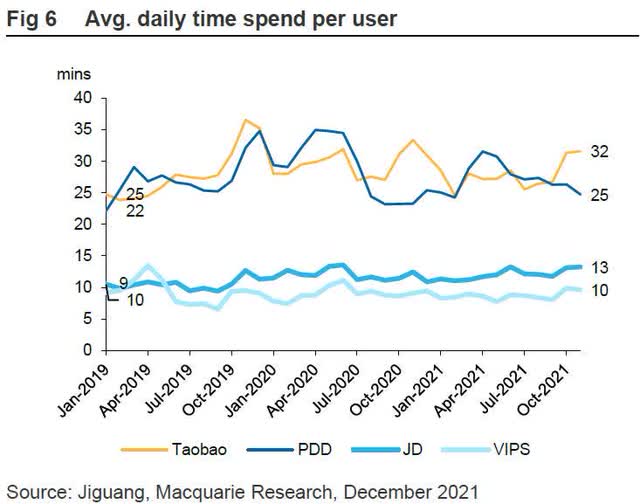

From the get-go, JD has a completely different market in mind. They focus on higher-quality goods and provide good fulfillment paired with good customer service to attract a certain “level” of the client. JD has much more of a premium aspect to its business than its peers.

This is evident from the following graphs which show that JD’s orders are on average multiples the value of competitors while spending much less time on the JD’s website compared to other services.

Macquarie Research Report Macquarie Research Report

JD Health

JD Health (OTCPK:JDHIF) has been trading on the HKEX since December 2020 and is the largest online healthcare platform in China. It is also included in the retail section.

JD has two clear advantages when it comes to the pharma retail part of the business.

- “Wealthier” Customers. As discussed earlier – JD customers generally spend more and on higher quality products when compared to its e-commerce rivals.

- Trust. JD’s reputation for being very stringent in terms of the quality of products they host on their platform serves them very well when it comes to pharmaceutical products.

JD Logistics

JD Logistics (OTCPK:JDLGF) went public in May 2021 and is also traded on the HKEX.

The logistics segment of JD’s business has been around since 2007. What has followed has been 15 years of investing in a loss-making division of the business – but developing and advancing it to a standard where it is arguably one of the most advanced supply chain solution companies in the world.

Breakeven for the logistics business is expected in Q42021. The high level of investment has enabled JD to develop sophisticated, automated machinery, automated delivery drones, big-data based software, etc. – enabling them to operate at a much more efficient level than peers.

JD.com IR

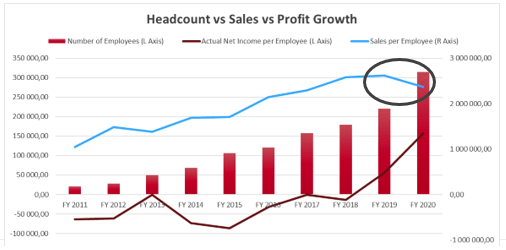

JD first opened the fulfillment infrastructure to 3rd parties in 2017. The share of revenue from external customers subsequently increased from 30% in 2018 to 43.4% in 2020. This wider adoption and greater utilization will have a positive effect on margins going forward.

While JD will continue to invest into new technology to stay at the forefront – I believe the level of investment will be going down from prior levels. From the graph below, we can see that JD has now reached a point where the sales per employee is not increasing anymore (circled).

Created by Author

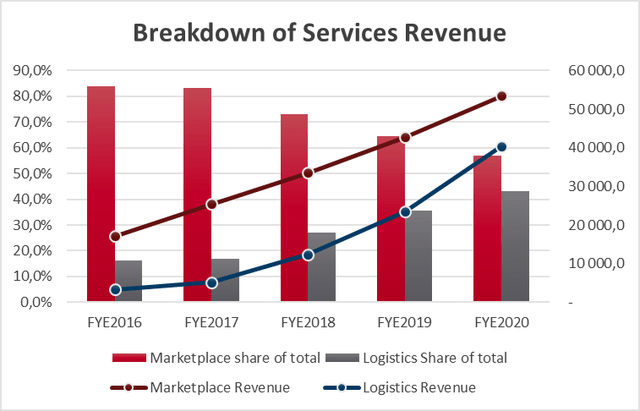

The logistics division has increased its share of service revenue at a rapid pace over the last five years, and it is continuing to grow at a faster rate than other segments. There was no stopping this trend during the first 9 months of 2021, as revenues from logistics and other services surged 74% on a YoY basis versus a total revenue increase of roughly 30% over the same period.

Created by Author

JD New Businesses

The main segments in the New Businesses Division are:

- JD Property

- JD Worldwide

- JD Technology

- Jingxi Business Group

JD Property was established in 2018 with the main goal of owning and operating JD’s logistics facilities and other real estate properties.

JD Worldwide is how international brands that are not readily available in China can get access to the market. It also aims to take quality Chinese products to the world.

JD Technology is basically JD’s fintech segment. JD.com owned about 37% of the JD Tech, but after a recent transfer of the Cloud and AI business to JD Tech, this stake was increased to 42%.

Jingxi is an e-commerce app that is dedicated to consumers in rural or lower-tier cities. Management has stated in recent quarters that 70-80% of new customers come from lower-tier cities – proving it was a good decision to invest in this area of the market.

How Big is the Addressable Market?

Chinese E-commerce Landscape

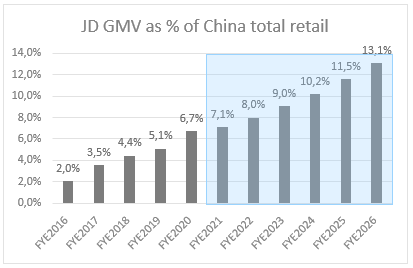

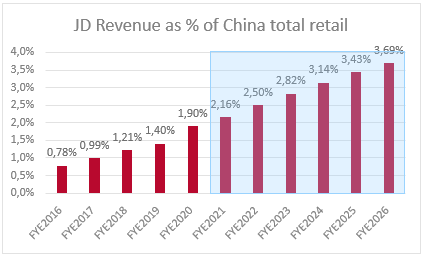

The size of China’s retail market in 2020 was 39.2 trillion RMB.

JD’s GMV as a % of the total retail market has been steadily rising for a number of years, from 2% in 2016 to 6.7% in 2020. For the forecast period in blue, Macquarie Research estimates that JD will be able to continue growing GMV at a CAGR of 19% through 2025, after increasing at a CAGR of 26.3% since 2017. I have grown the Chinese retail market at the same rate as their expected GDP growth, around 5% per annum, which might be conservative compared to some industry reports, such as the one from Technavio which projects a 9.84% CAGR.

Created by Author

Similarly, JD has been able to increase its own revenue at a much faster rate than the Chinese market as a whole.

Created by Author

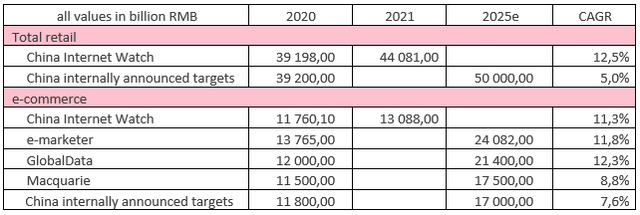

Collating data from a number of different sources yields the following:

Created by Author

- Total e-commerce in 2020: ± 12 trillion RMB

- Total e-commerce in 2025: ± 20 trillion RMB

Created by Author

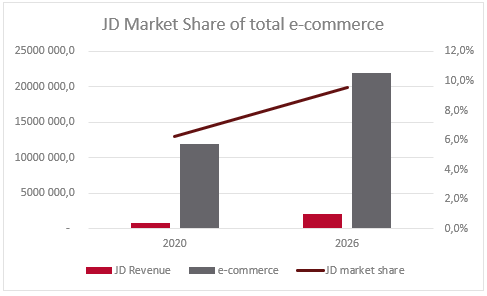

Based on my current revenue projections, JD will be increasing its market share from 6.2% to 9.5% by 2026.

Penetration Rates

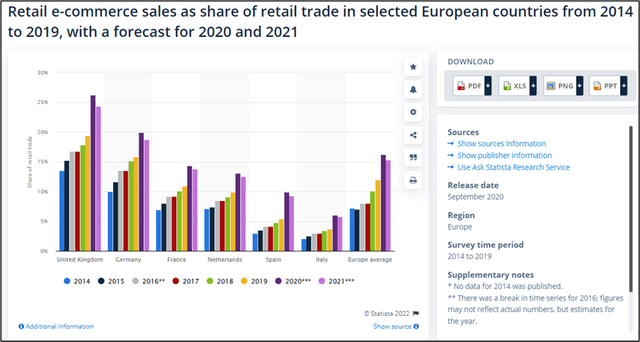

The e-commerce online penetration rate in China, at roughly 25-30%, is already fairly high compared to most of the world, with the global average at around 18%.

Statista

Even though penetration rates are already quite high, as evident from the graphs above, Bernstein expects online penetration to reach 40% within the next 5 years.

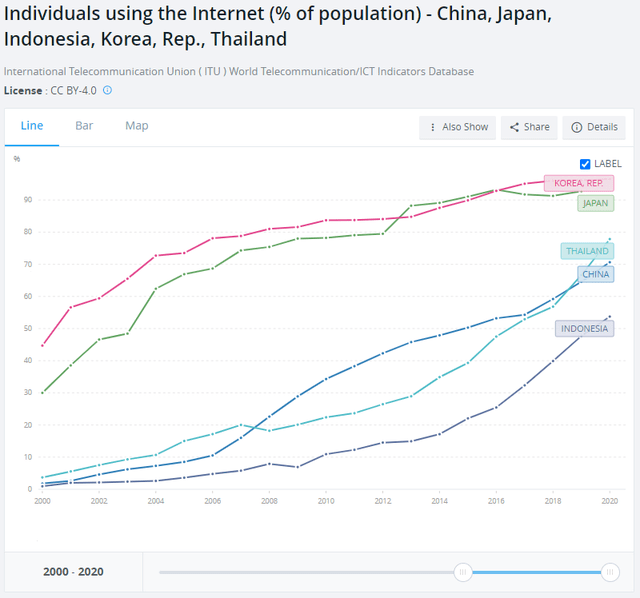

Further potential for growth is also evident when looking at internet penetration in China. According to data from the World Bank, this number currently sits just below 70% – with a much lower rate in rural areas. This is still a long way shy of the mid-90s penetration rate seen in both South Korea and Japan.

World Bank Data

Annual Active Users

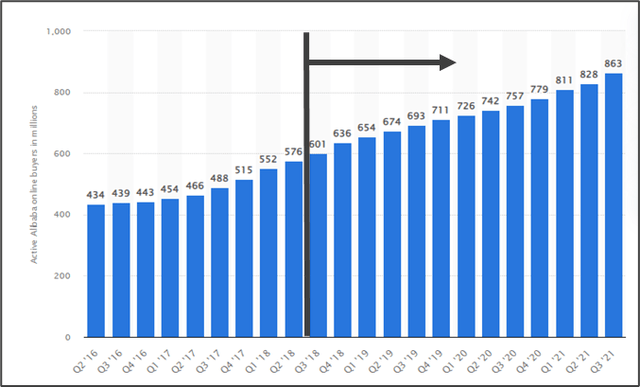

The number of active users of the Chinese platform companies is astounding. Between 2020 and 2021, JD added 111 million users.

A recent Macquarie Research report estimates that JD will continue growing at a rapid pace, with active customers reaching 719 million in 2022 and 830 million in 2023 – growing at 20% and 15%, respectively.

That would mean 2 more years of adding in excess of 100 million active users per annum. Considering how briskly Alibaba managed to move from JD’s current position (indicated by the vertical line below), I believe continued strong growth is attainable.

Statista

Rise of the Chinese Middle Class

In 2000, China’s middle class constituted roughly 3% of the population. By 2018 – more than 50% had entered the middle class. This almost puts it on par with the US, where 52% of the population is considered to be middle class.

There is, however, still a big difference between the two. While half of the Chinese population might now be classified as middle class, the other half would still be classified as low-income – whereas in the US the remaining 50% are classified as high-earners. I believe this will be a big driver of growth for JD going forward.

China Power

China Power China Power

There is also a big difference between the lower-middle class and upper-middle class. China has a very large lower-middle class – while this is much smaller in the US as well as Asian peers Japan and South Korea.

Regulatory Issues – The China Equation

There have been several reports and analysts recently questioning whether China is still investable, or whether the country should be avoided completely.

What is Xi’s goal? Does he want to rid China of every aspect of capitalism? No. A free-thinking, capitalist society stimulates technological advancement and economic growth – they are some of the most important aspects that enabled the formation of Chinese tech and retail giants.

JD Retail CEO, Xu Lei, stated during their Q2 2020 earnings review that China’s new regulations are not – as some investors fear – “intended to restrict or suppress the Internet and relevant industries”, but that, in fact, the goal was to create a “fair and orderly business environment and to promote long-term and sustainable development of these industries”.

During a key economic meeting in Beijing during December 2021, CCP leaders marked “stability” as their top priority for 2022 – a far cry from the previous year’s meeting, when the focus was “curbing the disorderly expansion of capital“.

However, after taking all of the above into account, no one knows exactly what the CCP’s next move might be, and investors need to be cognizant of the risks involved.

SWOT Analysis

Strengths

Logistics. Their logistics expertise certainly puts JD in a class of its own. The ability to deliver 90% of products within 1 day is unmatched. This is a very capital-intensive business to get off the ground, and JD has already done the hard yards. They are years ahead of any competitor in this space.

Authenticity. From day 1 – JD has focused on providing authentic products. I believe this has bought them loyalty and trust from customers.

Stickiness of Customers. Management indicated during their 3Q21 call that customers who stayed with JD for longer than 12 months tended to double the number of categories from which they purchase during the following year.

Negative Working Capital. JD collects their receivables in less than 3 days while only paying creditors in about 50 days.

JD.com IR

Table refers to Q320 to Q321

Weaknesses

Dual Class voting structure. Richard Liu holds more than 75% of the total voting power.

Lower margins. 1P businesses generally have much lower margins, and JD has a large 1P segment.

Limited International Growth. I do not believe JD will be as appealing to Western markets as they were in China, as many retailers provide high-quality products.

Opportunities

Capitalize on 3P. Merchants are now able to list on both Alibaba and JD, presenting JD with an opportunity to grow their 3P business.

Margin Expansion. Although JD has stated that investment will remain relatively high, this will gradually decrease, leading to margin improvement.

Lower-tier cities. Lower-tier cities are much less penetrated than upper-tier cities. JD has been adding many users in these areas of late, with as much as 80% of new users in the latest quarters coming from lower-tier cities.

JD Plus. JD’s subscription service has been around since 2015 – and currently only has 15 million members. Members are mostly young, educated professionals in Tier 1 and 2 cities and on average had ARPU that is 9 times higher than non-members.

Threats

Fierce competition. The Chinese e-commerce sector is highly competitive. Pinduoduo’s impressive growth indicates that the barriers to entry might not be as high as one would think. PDD managed to grow their annual active users from 245 million in 2017 to over 800 million presently.

Tencent (OTCPK:TCEHY) (OTCPK:TCTZF) shares. Tencent shareholders will be receiving their allotment of JD shares in May. This could lead to some selling pressure if new shareholders choose to unload.

Macro concerns. JD’s investment case has some macro elements to it. The Chinese train needs to keep rolling for companies like JD to keep growing.

VIE & Delisting. The possibility of liquidity issues as many mandates will not allow overseas investment, should any of the delisting fears materialize.

Valuation

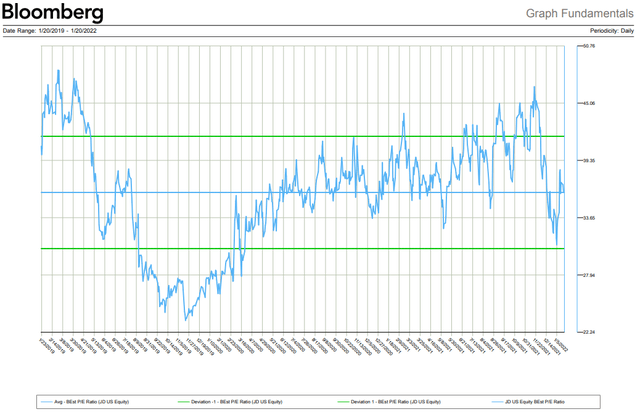

On a relative basis, JD seems fairly valued at the moment, trading at a blended forward P/E of 36, which is pretty much bang on its long-term average. The standard deviation lower band sits at 30 while the upper band sits at 41.

Bloomberg

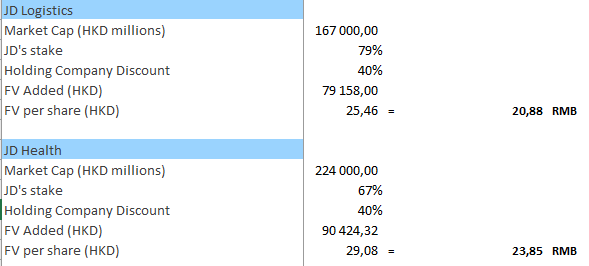

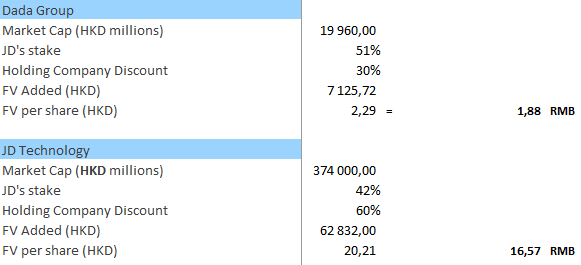

I used a sum-of-the-parts approach to value JD and affiliates. I applied a 40% holding company discount for JD Logistics and JD Health, a 30% discount to Dada Group – where JD’s stake is much smaller, and a 60% discount to JD Technology which is not yet listed.

Created by Author

Created by Author

Base Case: FV = 365 HKD, upside of 37%

- In my base case, I grow revenue at a CAGR of 17.2% over the next 5 years. The e-commerce market is expected to grow at a CAGR of ± 10%-12%.

- Regulatory fears persist, but to a lesser extent than seen in recent times with the gaming and education industries.

- I apply a mature earnings multiple of 17 – a premium to the average Chinese company – as JD is clearly better positioned than the average company.

Summary

JD has a strong moat – established by their focus on authenticity and their expertise in supply chain management. This will serve them well as the Chinese consumers will naturally move toward platforms offering higher quality products and better services as they move up the (common) prosperity ladder.