Table of Contents

Leila Melhado/iStock Editorial via Getty Images")

MercadoLibre, Inc (NASDAQ:MELI) is an online e-commerce marketplace that also provides payment services in Latin America. The company has two segments, Commerce and Fintech. The Commerce segment provides platforms to consumers in Latin America for purchases of goods and services, with advertising services for merchants to promote their listings. Meanwhile, the Fintech segment provides e-wallets for consumers with payment services that take advantage of the Commerce segment’s online sales.

In this analysis, we analyzed its positioning in the South American e-commerce market based on its market share and the overall market outlook in terms of rising internet penetration. We then projected its GMV based on the market forecast CAGR. Moreover, we examined its fintech segment growth outlook in terms of its positioning in digital payments and projected its revenue growth. Lastly, we analyzed its profitability which we expect to be hindered by rising logistics costs and forecasted its margins through 2026.

Exceptional Retail E-commerce Growth Provides Opportunity to Maintain Market Leadership

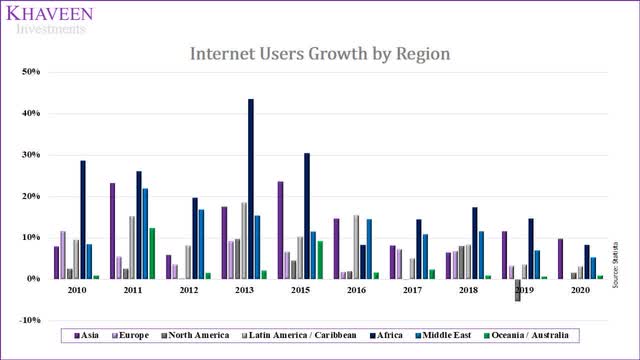

Latin America’s e-commerce share of retail sales was at 11% in 2020, one of the lowest compared to other regions and only ahead of the Middle East & Africa. However, in the same year, retail e-commerce companies in Latin America (MercadoLibre, B2W, Magazine Luiza (OTCPK:MGLUY) and Via Varejo) grew their GMV by 79%. Mercado’s market share in LATAM based on GMV was estimated at 25.40% in 2021. We believe that the reason behind the high e-commerce sales growth in Latin America could be due to Latin America’s relatively higher internet users growth at a 10-year average growth of 9.74%, compared to other matured major regions like North America (2.6%) and Europe (4.89%), according to data from Statista.

Statista, Khaveen Investments

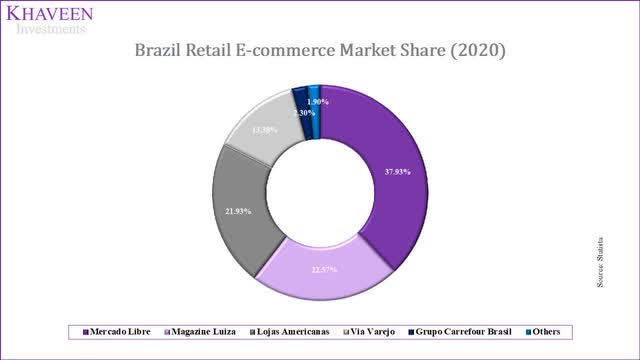

MercadoLibre derived 55.30% of revenue from Brazil in 2021 and was also the market leader in Brazil’s retail e-commerce market by GMV in the same year. MercadoLibre had 37.93% market share among the other competitors including Magazine Luiza, Logas Americanas, Via Varejo, Grupo Carrefour Brasil, and others. As the market leader in LATAM, we believe MercadoLibre stands to benefit from the retail e-commerce market growth in this region.

Statista

From 2022 onwards, we forecast its revenue/GMV % based on the 2021 figure at 16%. Besides that, we have also assumed MercadoLibre’s GMV to grow by 21%, according to Latin America’s e-commerce CAGR by Fidelity. Thus, we projected its marketplace revenue to grow to $8,918 mln by 2024.

|

MercadoLibre Revenue Projection ($ mln) |

2020 |

2021 |

2022F |

2023F |

2024F |

|

MercadoLibre GMV (‘a’) |

20,297 |

28,351 |

37,254 |

45,077 |

54,543 |

|

Growth % |

45% |

40% |

21% |

21% |

21% |

|

Revenue / GMV % (‘b’) |

13% |

16% |

16% |

16% |

16% |

|

MercadoLibre Marketplace Revenue (‘c’) |

2,560 |

4,635 |

6,091 |

7,370 |

8,918 |

|

Growth % |

90% |

81% |

31% |

21% |

21% |

*c = a x b

Source: MercadoLibre, Khaveen Investments

Fintech Segment Growth from the Low Banking Penetration

We believe that banking infrastructure is lacking in Latin American countries based on low banking penetration rates, with Mexico at 15% and Argentina at 9% in 2020. We further believe that Mercado’s payment system, Mercado Pago, is well-positioned to provide payment services and high payment volume growth, as shown in Latin America with a 5-year average growth of 90%.

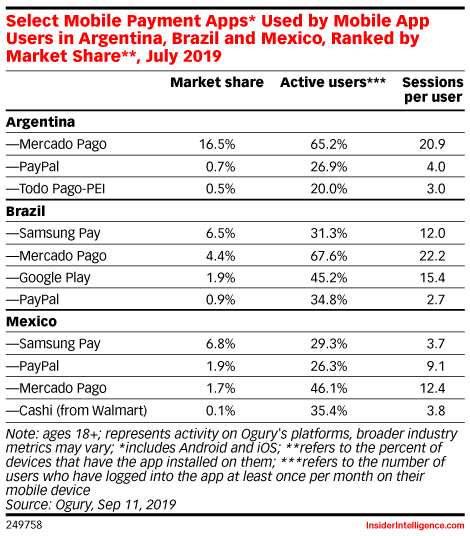

According to market research firm eMarketer, with QR code payment services launched in 2018, Mercado Pago had the first-mover advantage in Argentina, one of the countries with the lowest banking penetration rates. Its payment service provides fintech payment options which could make online shopping more widely available in the country by having the largest market share and active users share.

Based on the chart from eMarketer, the company still has the highest number of active users with the longest sessions per user in Brazil and Mexico. With the large user base, we believe Mercado Pago could generate more insights from user data and implement further improvements for the users, thus having the potential to increase its market share in the mobile payment application market in the future.

eMarketer

Moving forward, we expect the 70% growth of payment volume to remain through 2024. We have projected the Fintech segment revenue based on the payment volume growth rate of 70% and the 3-year average of Fintech Revenue / Payment Volume growth of -20%.

|

Fintech Revenue Projection |

2020 |

2021 |

2022F |

2023F |

2024F |

|

Payment Volume (‘mln’) (‘a’) |

1,915 |

3,255 |

5,533 |

9,406 |

15,989 |

|

Growth % |

128% |

70% |

70% |

70% |

70% |

|

Fintech Revenue / Payment Volume (‘b’) |

0.74 |

0.75 |

0.60 |

0.48 |

0.38 |

|

Growth % |

-35% |

1% |

-20% |

-20% |

-20% |

|

Fintech Revenue (‘c’) |

1,414 |

2,434 |

3,308 |

4,496 |

6,111 |

|

Growth % |

49% |

72% |

36% |

36% |

36% |

*c = a x b

Source: MercadoLibre, Khaveen Investments

Logistics Expansion Expected to Hinder Short-Term Profitability

While MercadoLibre is the market leader in the retail e-commerce marketplace in Latin America, the company has been facing negative earnings over the past 3 years. In the same period, the company’s cost of goods sold as a percentage of revenue has been increasing relative to revenue from 24.03% in 2016 to 46.56% in 2021.

|

MercadoLibre Cost of Goods Sold % |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

|

Revenue ($ mln) |

844 |

1,217 |

1,440 |

2,296 |

3,974 |

7,069 |

|

Growth % |

30% |

44% |

18% |

59% |

73% |

75% |

|

COGS as % of Revenue |

24.03% |

28.69% |

38.72% |

40.57% |

46.16% |

46.56% |

|

Growth % |

12% |

19% |

35% |

5% |

14% |

1% |

Source: MercadoLibre, Khaveen Investments

The company has mentioned its expansion in its logistics network and its impact on its bottom line in Q3 2021 earnings briefing.

We faced some bottom-line headwinds as we expand our first-party business and incur more operational costs while expanding our own logistics network. – Pedro Arnt, CFO MercadoLibre.

In Q4 2021, the company’s management provided an update and saw its logistics improving.

During this promotional season, we also saw improvements in our logistics network. During the fourth quarter, we shipped over 275 million items, while decreasing our average delivery times and simultaneously lowering average shipping costs per order. – Pedro Arnt, Chief Financial Officer

Mercado has been actively acquiring companies with collection and delivery points, for example, Kangu in August 2021. Besides that, the company also invests $1.1 bln in Mexico for storage and service capacity.

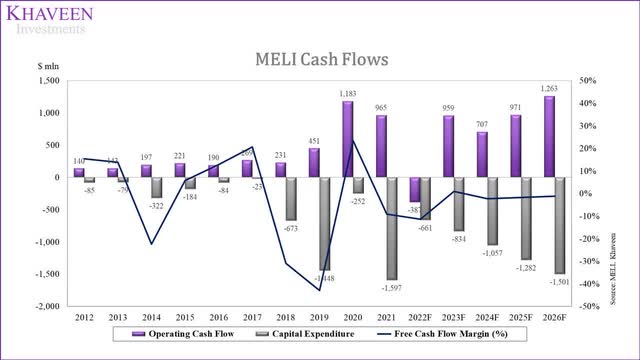

We projected the cost of goods sold in % of revenue to remain constant from 2022 onwards at 46.56% due to its expansion of shipping and logistics infrastructure.

Mercado Libre, Khaveen Investments

We assume that the company has the same days of accounts receivable as its inventory from 2022 onwards, at 13 days, and days of account payable to remain the same from 2022 onwards at 109 days. Due to the aggressive shipping and logistics expansion, we assume that the company could incur more capital expenditure at 7.0% of revenue from 2022 onwards.

Mercado Libre, Khaveen Investments

Risk: Competition in Payment Services

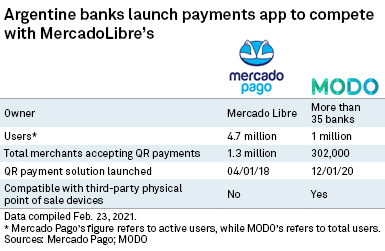

While MercadoLibre has the first-mover advantage in providing payment services benefited from the low banking penetration rate in Argentina, according to SP Global (SPGI), Argentine banks have launched payment applications to compete with Mercado’s payment app, Mercado Pago. The new payment application called Modo has been initiated by more than 35 banks in Argentina, with the benefit of being compatible with third-party POS devices. However, the total merchants accepting QR payments were still lesser compared to Mercado Pago as its application has the first-mover advantage in Argentina.

SP Global

MercadoLibre has taken initiative to strengthen its position in the payment services market in Latin America. In December 2021, MercadoLibre has announced its intention to acquire Redelcom, a POS provider to strengthen its strategy in Chile for SMEs and micro-entrepreneurs. This initiative could further increase the exposure of MercadoLibre to small businesses by providing merchants with detailed records of their transactions.

Valuation

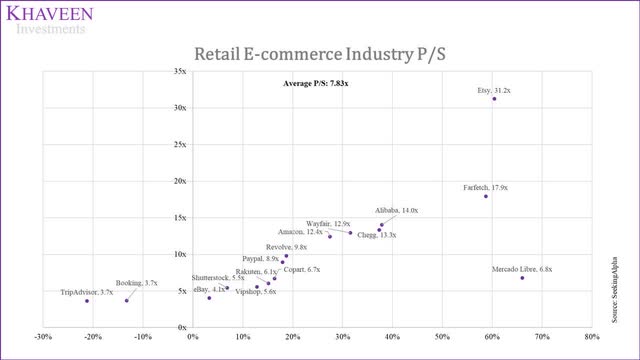

By taking selected retail e-commerce marketplaces and companies, we have an average P/S ratio of 7.19x.

SeekingAlpha, Khaveen Investments

We projected its marketplace revenue based on its GMV growth. We expect the Revenue / GMV % to remain at 16% from the 3-year average and MercadoLibre’s GMV to grow at 21%, Latin America’s expected retail e-commerce’s CAGR through 2024. Whereas for Fintech revenue, we expect MercadoLibre’s payment volume to grow at 36% from 2022 through 2024.

|

MercadoLibre Revenue Projection |

2019 |

2020 |

2021 |

2022F |

2023F |

2024F |

|

MercadoLibre GMV ($ mln) (‘a’) |

13,997 |

20,297 |

28,351 |

37,254 |

45,077 |

54,543 |

|

Growth % |

12% |

45% |

40% |

21% |

21% |

21% |

|

Revenue / GMV % (‘b’) |

10% |

13% |

16% |

16% |

16% |

16% |

|

MercadoLibre Marketplace Revenue ($ mln) (‘c’) |

1,346 |

2,560 |

4,635 |

6,091 |

7,370 |

8,918 |

|

Growth % |

61% |

90% |

81% |

31% |

21% |

21% |

|

Payment Volume (‘mln’) (‘d’) |

838 |

1,915 |

3,255 |

5,533 |

9,406 |

15,989 |

|

Growth % |

115% |

128% |

70% |

70% |

70% |

70% |

|

Fintech Revenue / Payment Volume (‘e’) |

1.13 |

0.74 |

0.75 |

0.60 |

0.48 |

0.38 |

|

Growth % |

-27% |

-35% |

1% |

-20% |

-20% |

-20% |

|

Fintech Revenue ($ mln) (‘f’) |

950 |

1,414 |

2,434 |

3,308 |

4,496 |

6,111 |

|

Growth % |

58% |

49% |

72% |

36% |

36% |

36% |

|

Total Revenue ($ mln) (‘g’) |

2,296 |

3,974 |

7,069 |

9,399 |

11,866 |

15,028 |

|

Growth % |

60% |

73% |

78% |

33% |

26% |

27% |

c = a * b

f = d * e

g = c + f

Source: MercadoLibre, Khaveen Investments

By taking the P/S industry average of 7.19x for our P/S valuation, we obtained an upside of 15% for its shares.

|

P/S Valuation |

2022F |

2023F |

2024F |

|

Revenue ($ mln) |

9,399 |

11,866 |

15,028 |

|

Growth % |

33% |

26% |

27% |

|

P/S Industry Average |

7.19x |

7.19x |

7.19x |

|

Valuation ($ mln) |

67,596 |

85,339 |

108,082 |

|

Shares Outstanding (‘mln’) |

50.42 |

50.42 |

50.42 |

|

Target Price ($) |

$1,341 |

$1,693 |

$2,144 |

|

Current Price ($) |

$1,161 |

$1,161 |

$1,161 |

|

Upside / Downside |

15.50% |

45.81% |

84.67% |

Source: MercadoLibre, Khaveen Investments

Verdict

MercadoLibre has demonstrated its capability to become the market leader in Latin America’s retail e-commerce market by having high revenue growth. It has further benefited by the countries’ room to grow with low e-commerce penetration rate and high e-commerce growth. The lack of banking infrastructure provides MercadoLibre with opportunities to offer consumers payment services with the company experiencing high growth of 90% on a 5-year average. However, the company has been experiencing a rising cost of revenue and it could be impacted in the short term by the expansion of its logistics.

Overall, given the potential of revenue growth by MercadoLibre, we have used P/S valuation and have a Buy recommendation, with a price target of $1,341.