Table of Contents

matdesign24/iStock by means of Getty Photos

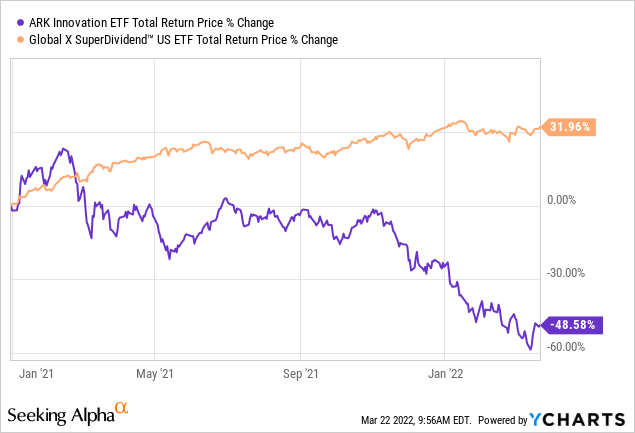

Higher Generate (DIV) has pummeled tech (ARKK) considering that we went over weight the significant produce benefit sector in late 2020:

The factors for this consist of:

- Tech shares bolstered by the Pandemic such as Zoom (ZM), Teladoc (TDOC), and Roku (ROKU) experienced only attained bubble-like valuations that have been not sustainable.

- The COVID-19 government restrictions and consumer anxiety started to lift in 2021 and that trend has accelerated in 2022 as the COVID-19 shots spread speedily and variants of the virus have gotten progressively much less extreme. This has boosted common corporations that endured from COVID-19 like bricks-and-mortar retail (SPG)(O), workplace properties (BXP), and strength providers (XOM) while getting rid of a big COVID-19 induced tailwind for online businesses like Amazon (AMZN).

- Inflation soaring to 4 ten years highs as a result of huge governing administration stimulus spending and intense source chain disruptions has forced plan makers to established a training course for climbing interest prices. As a end result, businesses whose intrinsic value largely rests in extended-dated cash flows have taken a beating. This disproportionately hit high advancement tech shares.

Even so, soon after the current tech crash there are some extremely eye-catching possibilities rising. Although I do not typically acquire tech shares specified my benefit and dividend investing focus, when I do, I obtain three that could improve the globe.

#1. Opendoor Technologies (Open)

At our mum or dad firm – Leonberg Capital – we are real estate buyers at coronary heart. Although we present in-depth protection of the REIT sector at our sister support Higher Generate Landlord, we also invest in serious estate alternatives at Higher Yield Trader. Thanks to major member desire, we have not too long ago introduced a distinctive sequence exploring eye-catching possibilities in the Assets Technological know-how room. Provided that large yield opportunities in this place are scarce at the second, we are unlikely to include any investments to our portfolios at Significant Produce Investor or Substantial Produce Landlord for the foreseeable long run. Having said that, we nonetheless wished to spotlight a few prospects for customers. We are specially intrigued in this house right now for the reason that:

-

Valuations in the room have turn out to be attractive in new months many thanks to the ongoing severe bear current market in tech/significant progress stocks.

-

Serious Estate constitutes the largest sector of the United States’ economic system with the GDP price additional of $1.898 trillion accounting for 13% of the nationwide GDP. It is also a person of the ripest sectors for technological disruption as there are a large amount of lingering inefficiencies and archaic practices in the industry. As a end result, the progress runway opportunity for PropTech companies is enormous.

- Some of the most revered and knowledgeable true estate traders in the world have just lately started pouring cash into this area. For illustration, one particular of our favorites – Brookfield Asset Administration (BAM) – lately invested $300 million into the sector.

BAM’s thesis listed here is to spend at the intersection of genuine assets and know-how disruption, providing strategic capital to superior growth technologies firms in order to accelerate efficiency and connectivity in the built surroundings. They are ready to leverage their in-depth know-how of the serious estate and authentic asset area to achieve an edge in the place and unlock considerable synergies by cross-offering expert services from these PropTech businesses and its large empire of authentic belongings.

As additional and extra major gamers devote in the space, we count on this to travel valuations increased and accelerate disruption of the real estate marketplace. Investing now when valuations stay minimal appears to be an attractive possibility-modified proposition.

One particular of our favored alternatives in this space is Open. Shopping for a house has extensive been considered as the cornerstone of the American Dream, but these days it is obtaining more challenging than at any time to achieve. Between soaring household rates, the menace of rising fascination premiums, and lingering high priced inefficiencies connected with the method (such as the hefty real estate agent costs and other burdensome buying and closing procedures and charges), home purchasing and providing stays a giant headache.

These hassles grow to be even additional obvious when put in the present day context of commerce, wherever the internet, cellular purposes, purchaser data, and stellar shopper provider are earning the shopping and selling encounters less difficult, speedier, and – in quite a few circumstances – cheaper than at any time. Real estate has been still left behind in this swift disruption and transformation, and OPEN’s mission is to push it forward into the fashionable age of world wide web and data run commerce.

We imagine that Open up is a compellingly intriguing expense chance correct now for the next factors:

- Robust business enterprise execution and performance monitor file

- Crystal clear aggressive rewards

- Large advancement runway

- Compelling situation for undervaluation

When Zillow (Z)(ZG) was at first our prime select in the house purchasing and providing room, due to the fact publishing our thesis final November, OPEN’s share cost has massively underperformed Z’s by a whopping 4,712 foundation details, shifting the valuation dynamic firmly in favor of Open in our watch.

Home Technological innovation is an underhyped option in our perspective and is positioned to generate sizeable price for the broader economic climate in the coming 5-10 decades. Earth-course real estate traders like BAM seem to be to believe that so as properly, more strengthening our conviction in the sector.

At the instant, Open appears to be like like a single of the additional promising options in the sector, as its iBuying enterprise design is fight tested and is clearly successful in opposition to rivals at the second. When other solutions like Z inventory were being additional pleasing late last 12 months from a valuation standpoint, OPEN’s inventory has because come crashing down to earth and features huge upside opportunity should it supply on analyst anticipations more than the following 50 percent decade.

The major threats to continue to keep in brain are the health of the housing current market and general market sentiment on expansion/tech stocks. Nevertheless, as extended as investors maintain a extended-time period viewpoint and management continues to control the harmony sheet and stock degrees prudently as they have hence much, Open up should really be in a position to conquer these two most important dangers and carry on to leverage its aggressive rewards to produce outsized lengthy-phrase returns. We watch Open as a speculative Powerful Invest in at present-day rates.

#2. Palantir Systems (PLTR)

Have you heard the expression “knowledge is the new oil?” Whilst oil has had a comeback currently because of to a re-opening overall economy, soaring inflation, and escalating geopolitical tensions, we believe that that the 21st century belongs to companies that master the art of harnessing and leveraging data.

One particular of the leading businesses in the industry of artificial intelligence and information analytics is PLTR. Their Gotham system – which services authorities-relevant businesses – is their main small business and carries on to increase at a robust clip. Provided the soaring geopolitical tensions and the accelerating A.I. arms race between the U.S. and China, PLTR is probably to continue taking pleasure in very solid demand from customers for its technologies and solutions from the U.S. Govt, govt contractors, and U.S. allies for several years to appear.

In the meantime, its Foundry platform – which services professional enterprises ranging from startups to top fortune 500 providers – is a much newer part of the business and is offering a sturdy extra advancement system. With innumerable issues facing corporations nowadays – especially with the critical provide chain issues confronting marketplace at the minute – PLTR’s systems and solutions are invaluable in enabling companies to harness knowledge and automation in purchase to make improvements to efficiencies and overall performance good quality concurrently.

When the stock has around halved in price tag in less than 5 months, the fundamental enterprise fundamentals continue being sturdy, with earnings anticipated to much more than triple over the following half 10 years and normalized earnings for each share to increase at a 40% CAGR over the exact time span.

Additionally, PLTR should be equipped to continue increasing at a significant amount for quite a few a long time to occur outside of 2026 as its whole addressable marketplace is now estimated to be at least $120 billion, which is substantial when you take into account that the enterprise is approximated to produce only a little around $2 billion in earnings in 2022. This indicates that even if PLTR have been to capture 5% of its overall addressable marketplace, it would triple its 2022 estimated income.

On major of that, PLTR’s full addressable market is not predicted to continue to be static in the coming yrs. In actuality, the world wide large information market is envisioned to improve at a CAGR of 22.4% via 2030. That means that all PLTR has to do is preserve its recent sector share and it will likely develop profits by 20%-25% yearly about the next decade. Even so, given its entrenched position in U.S. Govt agencies and contractors as properly as its promptly escalating community of partnerships in the company planet – together with with a selection of promptly escalating smaller innovators – we be expecting it to proceed grabbing industry share, building a 30%+ income CAGR pretty achievable via 2030.

#3. Coinbase World (COIN)

Last, but not least, COIN is on a mission to decentralize the global financial process by supplying folks access to competing decentralized mediums of exchange in an age when central banks are inflating fiat currencies into oblivion.

This by itself is a rationale to be bullish on cryptocurrency and COIN in specific, but other factors I am very long the stock include:

- COIN is the foremost, publicly traded cryptocurrency firm that is aggressively leveraging its substantial person and institutional networks, details benefit, and outstanding engineering to acquire and mature ancillary organizations to its cryptocurrency trading system such as NFTs, cybersecurity, and institutional storage expert services.

- COIN is performing tirelessly to develop into the ultimate 1-stop-shop and irreplaceable cryptocurrency ecosystem, proclaiming on a recent earnings connect with:

We want to be the Amazon of [crypto] belongings

- Unlike many other significant progress revolutionary tech firms, COIN is basically wildly financially rewarding, trades at a affordable valuation, and is employing its hard cash flows to make investments aggressively in advancing its technological abilities and rising new businesses centered on advancing the crypto financial system.

Investor Takeaway

Provided my worth and dividend investing roots, I overwhelmingly favor investing in hugely financially rewarding and a lot easier to understand companies more than selecting significant hazard, superior upside tech stocks that could see a vast array of probable outcomes in their foreseeable future.

HYI Financial investment Method

Some of my beloved substantial generate stocks at the instant that I have been obtaining aggressively just lately consist of Patria Investments (PAX) and Energy Transfer (ET) – two superior yield shares with strong stability sheets and huge upside prospective.

That stated, disruptive technological know-how has constantly fascinated me as an engineer and utilized mathematician and some stocks with extremely noble missions that could pretty quite possibly radically improve the entire world for the greater are now investing at interesting valuations. As a consequence, I have also been beefing up my tech publicity. By keeping a wholesome equilibrium in my portfolio when concentrating primarily on “heads I win, tails I don’t get rid of significantly” options in the dividend worth room, we have been capable to persistently beat the market place:

| HYI Core Portfolio | 54.8% |

| S&P 500 (SPY) | 21.7% |